What is Medicare?

Medicare is a federal health insurance program in the United States designed for individuals who are 65 years of age or older. It also covers younger individuals who have specific disabilities or medical conditions, including End-Stage Renal Disease (ESRD) or Lou Gehrig’s disease (ALS).

While this definition is quite simple, the Medicare program itself is complex, leading to ongoing confusion for many beneficiaries even after they sign up. Today, we aim to clear up that confusion for you!

Medicare was established in 1965 when President Lyndon Johnson signed the Medicare and Medicaid Act into law. This act created Medicare to provide health insurance for retired individuals. It also introduced Medicaid, which is frequently confused with Medicare. However, Medicaid is a separate health insurance program intended for people with limited incomes, regardless of age.

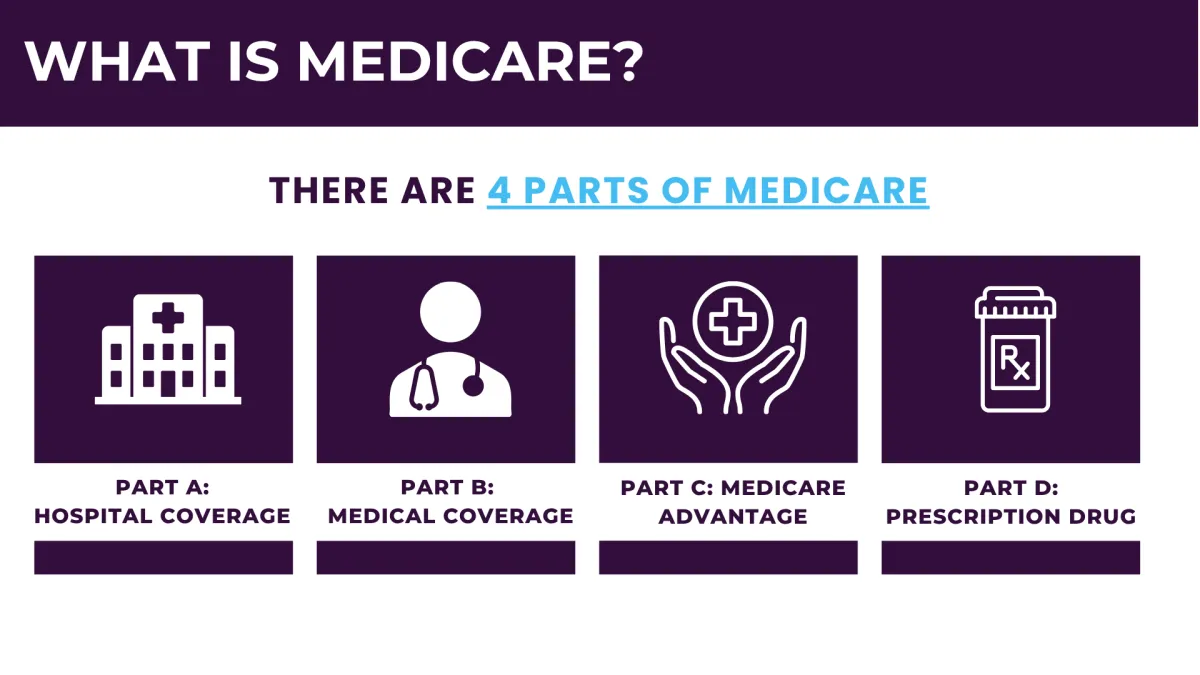

The Medicare program is divided into four parts, with additional options for extra coverage. Everyone begins with Parts A and B, while the other parts depend on personal healthcare needs and budget considerations.

What are the different parts of Medicare?

Original Medicare

Original Medicare, sometimes referred to as Traditional Medicare, comprises Part A and Part B. This is the foundational coverage that everyone begins with. You need to enroll in both Parts A and B before you can opt for any additional coverage.

Part A

Medicare Part A, also known as inpatient or hospital insurance, covers inpatient hospital stays, care in skilled nursing facilities, hospice care, and some home health services.

Most beneficiaries do not have to pay a premium for Part A. If you or your spouse have worked and paid taxes for at least ten years (40 quarters), you qualify for premium-free Part A. If you haven't met this requirement, your premium is determined by the number of quarters you've worked, and these premiums typically increase each year.

Although Part A doesn't have a premium for most, there are other out-of-pocket expenses. It includes a deductible, which is not annual but instead applies to benefit periods. A benefit period starts the day you are admitted as an inpatient and ends after you have been out of the hospital or other facility for 60 consecutive days.

There are also copays for Part A, which depend on the length of your hospital stay. Medicare covers the first 60 days of hospitalization completely, but copays start accruing from day 61 onwards.

Part B

Medicare Part B, also known as outpatient or medical insurance, covers doctor visits, imaging, lab tests, surgeries, durable medical equipment, and many preventive care services.

Part B requires a monthly premium, which is set annually by the Centers for Medicare and Medicaid Services (CMS). Most people pay the standard premium, but those with higher incomes will pay more. Beneficiaries with limited incomes may qualify for Medicare Savings Programs to help cover the Part B premium.

There is also an annual deductible for Part B, which is relatively small. After meeting this deductible, Part B covers 80% of approved services, leaving beneficiaries responsible for a 20% coinsurance.

Unlike traditional group health insurance, Original Medicare does not have an out-of-pocket maximum. While it provides extensive coverage, this lack of a cap can result in significant financial burdens for beneficiaries.

Part C

Part C is mostly referred to as Medicare Advantage. To enroll in a Medicare Advantage plan, you must first sign up for Original Medicare. However, once enrolled, a private insurance company, rather than the federal government, provides all your benefits.

Medicare Advantage plans offer at least the same coverage as Original Medicare and often provide additional benefits

.For instance, you can include prescription drug coverage in your Medicare Advantage plan without an extra premium. Many plans also offer coverage for hearing, vision, and dental care, as well as wellness programs, gym memberships, transportation, meal delivery, and monthly over-the-counter stipends.

If you're considering Medicare Advantage, it's crucial to understand how these plans operate and explore the different options available. Medicare Advantage plans come in various types, so working with an advisor can help you find the one that best meets your needs.

One of the most appealing aspects of Medicare Advantage plans is their premium. Most Part C plans have very low monthly premiums, often as low as $0 per month. However, it's important to review the plan's out-of-pocket costs, including deductibles and copays.

Part D

Medicare Part D provides prescription drug coverage, which is not included in Original Medicare. To get coverage for your medications, you need a separate Part D policy, even if you aren't currently taking any prescriptions. Not enrolling in Part D can result in lifetime financial penalties.

Part D plans are sold by private insurance companies and can vary by region. When choosing a Part D plan, you should compare their drug formularies to determine which plan covers your medications at the lowest cost.

Understanding Medicare Enrollment Periods

Possibly one of the most confusing things about Medicare is all the enrollment periods. As confusing as they may be, they’re also critically important. Missing one could cause you to be without coverage, or you could even be subject to late enrollment penalties.

Today, we’re going to list all the Medicare enrollment periods you should be aware of. You may not need to utilize all of them, but you should know a little about each one so you can take advantage of them if need be.

Initial Enrollment Period

Your Initial Enrollment Period (IEP) is tied to your 65th birthday month. It starts three full months before your birthday month and ends three full months after it.

For instance, if your birthday is on July 2, your IEP runs from April 1 to October 31. If you enroll before your birthday month, coverage can begin on the first day of the month you turn 65, meaning your Medicare would start on July 1 in this example.

There is one exception: if your birthday falls on the first day of the month, your IEP starts a month earlier. For example, if your birthday is on July 1, your IEP would begin on March 1, and your Medicare coverage would start on June 1.

During your IEP, you should enroll in Parts A and B and consider any additional coverage you might need, such as a Medicare Supplement plan, a Medicare Advantage plan, or Medicare Part D.

Planning ahead for your IEP is crucial. Missing this enrollment period could lead to a lapse in coverage and incur late enrollment penalties. The only way to avoid this is to have other creditable coverage in place.

Creditable coverage typically comes from an employer-sponsored group health plan. If your employer has at least 20 employees, their health insurance is considered creditable. This allows you to postpone Medicare enrollment without penalties. However, always confirm with your advisor or HR director before making this decision.

Medigap Open Enrollment Period

Medigap, also known as Medicare Supplement plans, provides additional coverage for expenses not covered by Original Medicare. The Medigap Open Enrollment Period begins on the effective date of your Part B coverage and lasts for six months. This is a one-time enrollment period.

While Medigap plans are optional, they are a popular choice for supplementing Original Medicare coverage. Most people opt for either a Medigap plan or a Medicare Advantage plan. It's important to note that if you don't enroll in a Medigap plan during your Open Enrollment Period, you will need to pass medical underwriting to get a Medicare Supplement plan later, unless you qualify for an exception.

If you missed your Medigap Open Enrollment Period but are still interested in a Medigap plan, call Guardian Insurance Group for guidance on your options.

Medicare Advantage Open Enrollment Period

The Medicare Advantage Open Enrollment Period is an annual window that runs from January 1 through March 31. This period is specifically for beneficiaries who are already enrolled in a Medicare Advantage plan. During this time, you can make a one-time change to your Medicare Advantage plan or switch back to Original Medicare. If you choose to change your plan, the new coverage will take effect on the first day of the following month. If you switch back to Original Medicare, you can also use this time to enroll in a Part D plan for prescription drug coverage. Understanding these enrollment periods is essential to ensure you have the coverage you need. Call to speak with a trusted advisor to discuss your options.

Annual Enrollment Period

Medicare’s Annual Election Period (AEP) is one of the most crucial enrollment periods for all beneficiaries. Regardless of the type of Medicare plan you currently have, it's essential to mark your calendar for AEP.

AEP occurs annually from October 15 to December 7. During this period, you can make several changes to your Medicare coverage, including:

- Switching from one Medicare Advantage plan to another

- Switching from one Part D plan to another

- Changing from Medicare Advantage to Original Medicare

- Changing from Original Medicare to Medicare Advantage

Any changes made during AEP will take effect on January 1 of the following year.

AEP is vital because Medicare Advantage and Part D plans operate on annual contracts, and while your plan will automatically renew if you do nothing, the plan's specifics often change each year. These changes can include adjustments to premiums, deductibles, cost-sharing amounts, and benefits. For instance, a medication you have been taking for years may no longer be covered by your plan, or you might find a new plan with lower copays.

Even if you do not plan to make any changes, it's important to review your plans during the Annual Election Period. Guardian Insurance Group can help you stay updated on any changes to ensure you continue to have the coverage you need. Use our expertise to review your options and confirm that your current plan still meets your healthcare needs.a

Special Enrollment Periods

Special Enrollment Periods (SEPs) are designated for significant life changes, qualifying you for a period to make changes to your Medicare coverage. The actions you can take during an SEP depend on your specific situation. Common events that trigger an SEP include getting married or divorced, losing a spouse, losing income, or moving to a new service area. One of the most frequent reasons for qualifying for an SEP is continuing to work past the age of 65 while being enrolled in creditable insurance.

Another common reason for an SEP is moving out of your current plan’s service area. Since Medicare Advantage and Part D plans operate within specific service areas and provider networks, moving outside your current area gives you a two-month window to find a new plan in your new location.

There are many situations that might qualify you for an SEP, so it's always worth asking. We can help you determine if you qualify and guide you through the process.

You Don't Have to Figure This Out Alone

Medicare comes with a lot of moving parts—Advantage plans, Supplements, drug coverage, costs, benefits, networks, deadlines. Let us make this easy. Book your appointment today and get clear, personalized guidance so you can choose the right coverage with confidence.

What are you options after starting Medicare?

Add a Medicare Supplement Plan (Medigap)

A Medicare Supplement, also known as Medigap, is a type of health insurance policy sold by private companies designed to fill the gaps in Original Medicare coverage. While Original Medicare (Parts A and B) covers many healthcare costs, it doesn't cover everything. There are out-of-pocket expenses such as copayments, coinsurance, and deductibles that can add up.

Medigap policies help pay for these extra costs. For example, if you have a hospital stay, Medicare Part A will cover a large portion of the cost, but you might still be responsible for a deductible and daily coinsurance charges if your stay extends beyond a certain period. A Medigap policy can cover these additional costs, reducing your financial burden.

Medigap plans are standardized and labeled by letters A through N, each offering a different level of coverage. These plans are regulated to ensure they provide consistent benefits across different insurers, so a Plan G from one company will offer the same basic benefits as a Plan G from another company. However, premiums may vary between companies and locations.

To enroll in a Medigap policy, you must first have Medicare Part A and Part B. Medigap policies only cover one person, so if you and your spouse both want Medigap coverage, you each need to buy separate policies.

Medigap policies do not cover prescription drugs, so if you need drug coverage, you will need to enroll in a Medicare Part D plan separately. Additionally, Medigap does not work with Medicare Advantage Plans (Part C); if you have a Medicare Advantage Plan, you cannot use a Medigap policy.

Add a Medicare Advantage Plan

A Medicare Advantage Plan, also known as Medicare Part C, is an alternative way to receive your Medicare benefits through a private insurance company approved by Medicare. While Original Medicare (Parts A and B) provides essential coverage for hospital and medical services, Medicare Advantage bundles those benefits together and often includes additional coverage that Original Medicare does not provide.

With a Medicare Advantage Plan, you still have Medicare—it just works differently. Instead of receiving your benefits directly from the federal government, you receive them through a private insurer. These plans are required to cover everything Original Medicare covers, but many offer more. Depending on the plan, you may get added benefits such as prescription drug coverage, dental, vision, hearing, gym memberships, and other wellness extras.

Medicare Advantage Plans typically operate through provider networks, such as HMO or PPO structures. This means your out-of-pocket costs, premiums, and choice of doctors may vary based on the type of plan and the network it uses. Many Medicare Advantage Plans offer low monthly premiums—even as low as $0—but costs for services like copays and coinsurance can differ from plan to plan.

To enroll in a Medicare Advantage Plan, you must have Medicare Part A and Part B and continue paying your Part B premium. When you join a Medicare Advantage Plan, you receive your Part A and Part B benefits through that plan, and you cannot use a Medigap (Medicare Supplement) policy with it.

Most Medicare Advantage Plans include prescription drug coverage, eliminating the need to purchase a separate Part D plan. However, if you choose a plan that does not include drug coverage, you cannot enroll in a standalone Part D plan unless the plan type specifically allows it (such as certain PFFS plans).

Medicare Advantage is designed to offer a more all-in-one approach with potentially lower upfront costs and extra perks, making it a popular option for those seeking convenience and comprehensive coverage in one plan.

Conclusion

Choosing the right Medicare plan is a personal decision that depends on your individual healthcare needs, budget, and lifestyle. Whether you prefer the flexibility of Original Medicare with a Prescription Drug Plan, the comprehensive coverage of a Medicare Supplement, or the additional benefits of a Medicare Advantage plan, the best choice varies from person to person.

We understand that navigating Medicare options can be confusing. That's why we're here to help you make an informed decision tailored to your unique situation.

Call today to get help! Our experts are ready to assist you in finding the perfect Medicare plan for your needs.

You Don't Have to Figure This Out Alone

Medicare comes with a lot of moving parts—Advantage plans, Supplements, drug coverage, costs, benefits, networks, deadlines. Let us make this easy. Book your appointment today and get clear, personalized guidance so you can choose the right coverage with confidence.

Medicare Information

COMPANY

LEGAL

SOCIALS

As a national Medicare brokerage, we work with multiple carriers to provide comprehensive plan options. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options. This is not a complete listing of plans available in your service area. For a complete listing please contact 1-800-MEDICARE (TTY users should call 1-877-486-2048), 24 hours a day/7 days a week or consult www.medicare.gov.

Copyright 2026. Guardian Insurance Group LLC. All Rights Reserved.